- Artificial intelligence is driving significant growth in the semiconductor industry, with revenues projected to reach nearly a trillion dollars by 2029.

- Intel and Nvidia are key players in the semiconductor market, offering distinct investment narratives.

- Intel faces challenges, including a $19.2 billion net loss and production cost issues, but seeks revival through custom chips and new innovations like the Panther Lake chip.

- Nvidia leads in AI chipsets, achieving a 114% revenue increase in fiscal 2025, driven by its Blackwell Ultra platform.

- Investors face a choice between Intel’s potential long-term turnaround and Nvidia’s immediate growth and resilience.

- Nvidia is poised as the leading force in the AI semiconductor industry, offering strong prospects for future success.

The digital realm is buzzing with the promise of artificial intelligence, sparking a surge in the semiconductor industry that has investors reaching for their wallets. The sector witnessed a meteoric rise, achieving a remarkable 19% growth in revenue to $627 billion in 2024, with forecasts predicting a leap to nearly a trillion dollars by 2029.

At the heart of this techno-gold rush stand two titans: Intel and Nvidia. Each embodies a distinct narrative in the semiconductor saga, beckoning investors to ponder where their gains might lie. Historically, Intel ruled the personal computing world, its legacy stretching across decades. However, Nvidia has emerged as a frontrunner in the AI chip renaissance, its cutting-edge technology captivating the industry.

Peering through the lens of Intel’s current state unveils a complex tableau. The company’s shares suggest a bargain, with a price-to-book ratio signaling undervaluation. Yet, beneath the surface, challenges simmer. Revenue has dwindled and Intel’s fiscal standing suffered a harsh blow with a $19.2 billion net loss as 2024 drew to a close. The downturn is largely due to its foundry business facing turbulent times. With foundries of its own, Intel feels the strain of increased production costs—a burden Nvidia sidesteps by outsourcing chip fabrication.

Notwithstanding this turbulence, Intel’s resolve remains firm. It launched new ventures, fabricating bespoke chips for behemoths like Microsoft and Amazon, as they both pivot toward customized AI infrastructures. Moreover, Intel’s semiconductor line reported modest revenue growth, and its latest innovation, the Panther Lake chip for PCs, is poised to enter the fray, potentially revitalizing its fortunes.

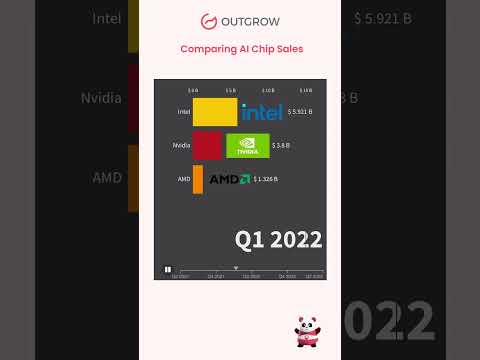

On the other hand, Nvidia rides high on a wave of innovation and sales success. It shattered expectations with $130.5 billion in revenue in fiscal 2025, vaulting 114% from the previous year. Nvidia’s secret weapon lies not in the grounding stones of foundries but in its visionary AI chipset leadership. Its cutting-edge Blackwell Ultra platform epitomizes the frontier of AI development, fostering a new era of AI reasoning that promises to transcend traditional pattern recognition.

Tech giants have already begun clamoring for Nvidia’s transformative platform, which is an essential tool for the computing power demands modern AI applications impose. Consequently, Nvidia’s financial outlook appears nothing less than stellar, projecting it as a compelling choice for the forward-thinking investor.

Yet, deciding between these semiconductor stalwarts isn’t a simple affair. Intel’s stock may be tempting given its potential for a turnaround, especially under the fresh leadership of Lip-Bu Tan. Nevertheless, such transformations are rarely swift, demanding sustained strategic shifts over years.

Conversely, Nvidia exemplifies growth and resilience. Its stock may have recently dipped, but the trajectory suggests it’s merely a pause. Investors looking for assured returns in the exploding AI sector might find Nvidia’s strong performance and future roadmaps too promising to ignore.

Hence, while Intel offers a prospective turnaround tale for the patient investor, Nvidia stands out as the semiconductor star likely to shine brightest, leading the revolution in AI technology. As it marries cutting-edge innovation with robust financial health, Nvidia embodies the future of semiconductor success in the age of artificial intelligence.

The Unstoppable Rise of AI Semiconductors: Nvidia vs. Intel

Overview

In the ever-evolving landscape of artificial intelligence and semiconductor technology, the battle for dominance between Intel and Nvidia takes center stage. As the semiconductor industry looks to achieve a staggering growth to nearly a trillion dollars by 2029, investors are keen to decipher which titan offers the most promising returns.

Key Insights

1. The Semiconductor Market Forecast

– Exponential Growth: The semiconductor industry is poised for exponential growth, with projections emphasizing a significant leap to $627 billion in revenue by 2024. This surge will cater to burgeoning demands across AI, automotive, and consumer electronics sectors.

– Industry Trends: A driving trend is the increasing integration of AI and machine learning applications, which require advanced semiconductors designed for rapid data processing and energy efficiency. Gartner notes that AI chipsets are not just a trend but a fundamental shift in technology infrastructure.

2. Intel’s Challenges and Outlook

– Current Struggles: Intel faced a critical $19.2 billion net loss in 2024, largely due to rising production costs and challenges in its foundry business. However, efforts to diversify by fabricating bespoke chips for Microsoft and Amazon indicate a strategic pivot toward AI infrastructure.

– Strategic Initiatives: Under new leadership, Intel has launched the Panther Lake chip, aiming to revamp its position in the PC market. Its appeal lies in potential long-term gains, especially if these ventures prove successful.

3. Nvidia’s Triumphant Surge

– Sales and Innovation Success: Nvidia reported $130.5 billion in revenue in fiscal 2025. Its growth is anchored in its Blackwell Ultra platform, which is pushing the boundaries of AI development and computing power.

– Investor Appeal: With visionary leadership in AI chipsets and significant demand from tech giants, Nvidia projects robust financial health. This positions it as an attractive choice for those focused on growth and innovation.

How to Decide: Intel vs. Nvidia

Pros and Cons Overview

– Intel: Offers potential for a turnaround with undervalued stock and strategic new ventures. However, it requires patience as transformations take time.

– Nvidia: Provides immediate growth potential with proven financial success and elite technology. It remains a preferred choice for investors seeking involvement in the AI boom.

Real-World Use Cases

– AI Development: Nvidia’s chipsets are perfect for AI applications such as autonomous vehicles and data centers, which require immense processing power.

– Custom Chip Fabrication: Intel’s move to create custom chips caters to companies like Microsoft and Amazon seeking unique AI solutions. This flexibility could become a significant revenue stream.

Predictions and Recommendations

Insights & Predictions

– Nvidia’s Dominance: Given current trends and innovative prowess, Nvidia is likely to continue spearheading growth in the semiconductor market, driven particularly by expanding AI applications.

– Intel’s Recovery: Although challenging, Intel’s recovery hinges on the success of strategic initiatives around AI infrastructure and new leadership effectiveness.

Actionable Recommendations

– Nvidia: Consider investing in Nvidia for short-to-medium term gains, particularly if seeking exposure to the expanding AI sector.

– Intel: For those willing to embrace risk and a long-term horizon, Intel provides a potential undervalued investment opportunity, especially as new product cycles unfold.

For more insights on technology investments, visit CNBC.

By weighing market trends, company prospects, and strategic initiatives, investors can make informed decisions about where to place their bets in the dynamic AI-driven semiconductor industry.